Cracking Box #19 — What It Means for Your Pension

What Box #19 on your LES is, why it matters, and how it connects to the FERS refund you may be eligible to claim.

Mark Brown

October 3, 2025 · 7 min read

This is the first article in a series that will break down the components of a Leave and Earnings Statement (LES). The purpose of the series is to explain important pay, retirement, and benefits-related concepts to ensure you can track, understand, and receive all of your earned benefits.

Box #19 on your LES is often overlooked and rarely understood. This article will explain what it means and why it matters.

What is Box #19?

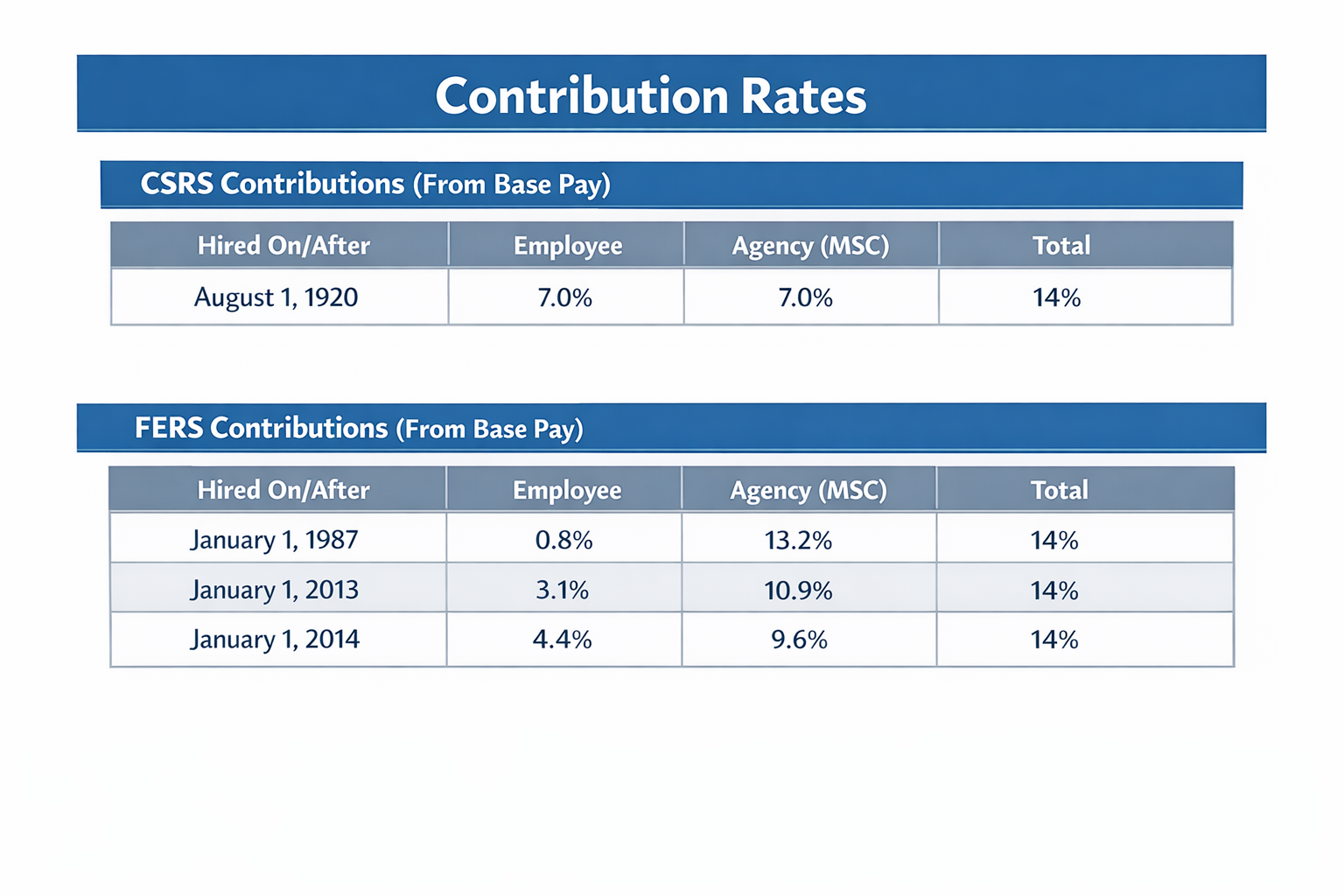

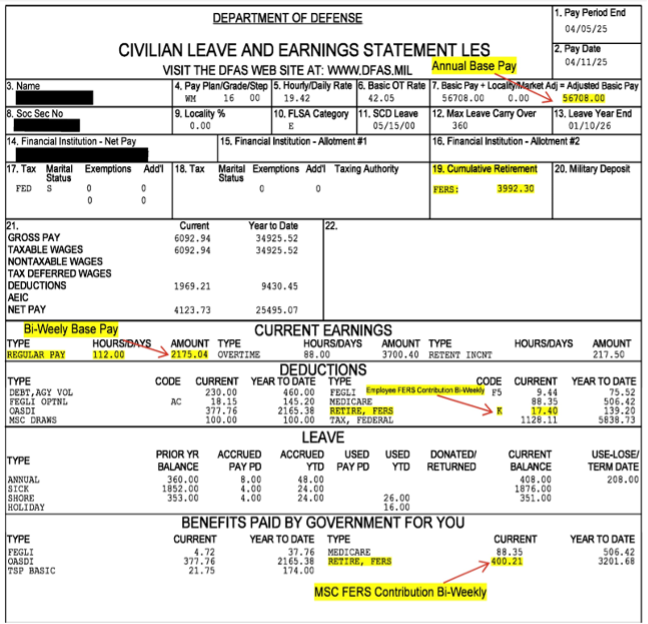

Box #19 is the "Cumulative Retirement" box. Each pay period, a percentage of your base pay is automatically deducted and contributed to the retirement system. The number in Block #19 is the total dollar amount of employee contributions you have made to the Federal Employee Retirement System (FERS) to date while under the current Pay Center.

The cumulative retirement contributions in Box #19 define the amount of your FERS or CSRS retirement annuity (CIVMAR Pension) that is tax-free, as these were made as "after-tax" contributions. The cumulative amount does not include Agency (MSC) contributions. This is not the same as the monthly pension you will receive in retirement—it is your personal contribution to the retirement fund.

Key point: Box #19 represents your after-tax contributions (your "basis"), which are later recovered tax-free during retirement. It does not mean your entire annuity is tax-free. The tax-free portion is determined by your cumulative employee career contributions to FERS or CSRS.

These contributions are deducted from BASE PAY (which will be explained in next month's article). Base Pay changes for many reasons, including receiving Ship Pay, Pool Pay, a promotion, Cost of Living Adjustments (COLAs), and more.

If you transfer to a different agency, the cumulative amount will reset to $0.00, but your total federal service record and contributions to FERS or CSRS will be maintained by the Office of Personnel Management (OPM).

An Important Note for Those Hired Before June 1, 2014

If you were hired prior to June 1, 2014, the amount in Box #19 will not reflect your full career contributions. Military Sealift Command changed its pay center to the Defense Finance and Accounting Service (DFAS) on June 1, 2014. This transition moved the payroll function from the MSC Unified Civilian Mariner Payroll System (UCPS) to the DFAS-managed Defense Civilian Pay System (DCPS).

OPM will assimilate your total FERS contributions as part of finalizing your retirement, as they maintain all your payroll records.

Cumulative contributions on an LES start over when:

- The Pay Center changes (as it did with MSC in 2014)

- You change the agency you work for

- You resign and later return to MSC or any other Federal Agency

Your total contributions are still recorded—but the number on your LES will start over.

The combined cumulative contributions fund defined benefit plans where the government pays your pension from its own retirement funds, like the Civil Service Retirement and Disability Fund (CSRDF). Your federal pension (annuity) is a promise from the government to provide guaranteed lifetime income based on your years of service and salary history.

In other words: Your retirement annuity is a percentage of your Average High-3 (highest three consecutive years) of Base Pay. We'll dive deeper into Average High-3 and Base Pay in future articles.

Your Options If You Leave Federal Service

Not every CIVMAR will retire from MSC. Family, health, logistics, or other issues may prevent you from continuing in your seagoing position. If you resign (not retire) from Military Sealift Command, you need to consider your options for the funds in Box #19.

Option 1: Continue Federal Employment

Move to a shore-based position with MSC or any other Federal Agency. You'll continue having FERS contributions deducted from your pay and continue working toward a federal retirement.

Option 2: Resign and Apply for Deferred Retirement

You can apply for a deferred retirement at the following ages and years of service:

- Minimum 5 years — Eligible at age 62

- Minimum 10 years — Eligible at age 56–57 (depending on birth year)

A deferred retirement provides a permanent FERS Annuity (pension) and a Survivor Benefit option for life. However, you would not be eligible for Health & Life insurance benefits.

Alternative: Leave your cumulative retirement contributions in place. If you return to MSC or any other Federal Agency in the future, you can be credited the prior service time and contributions toward a full retirement. This is known as a "break in service." Upon return, your Service Computation Date (Box #11) would reflect your prior service.

Option 3: Withdraw the Money

To request a FERS contribution refund:

- Complete the Application for Refund of Retirement Deductions (FERS), Standard Form (SF) 3106, from the OPM website

- If separated for 30 days or less, submit to your servicing personnel office

- If separated for more than 30 days, mail the completed application to the OPM Retirement Operations Center in Boyers, PA

Interest on refunds:

- For FERS service over one year, you receive interest at the same rate paid for government securities

- For CSRS service between one and five years, interest is paid at 3%

Rollover options:

You can roll over lump sum payments (retirement contributions, voluntary contributions, and applicable interest) to an IRA or employer-sponsored plan. The government is required to withhold 20% Federal income tax from taxable payments over $200—but if you choose a direct rollover, no tax is withheld.

You have 60 days after receiving a payment to roll it over. You can roll over up to 100% of the eligible distribution, including replacing the 20% withholding out of pocket. You will be taxed on any amount you do not roll over.

Caution: Think Before You Withdraw

Your TSP is separate. Your Thrift Savings Plan value is yours and can be left in place, cashed out, or rolled into an outside IRA or employer-sponsored plan. If you resign without at least three years of service, you are not vested in the matching of up to 5%. TSP will be discussed in a separate article.

If you withdraw retirement contributions, be certain you are not returning to Federal Service.

If you return after withdrawing, your prior service does not exist. You can re-deposit the money to "buy" back the prior service, but you will owe interest that compounds annually.

If you started with MSC prior to June 1, 2014, expect an additional 2–4 months for payout of Box #19, since totals from two Pay Centers must be assimilated by OPM through the archives.

In my 22 years of working with Federal Employees, I have seen many who resign from Military Sealift Command return to Federal service for any number of reasons. In most cases, it was—or would have been—better to leave FERS retirement contributions in place until you are certain you are not returning. The previous service credit time was more valuable upon return than the money withdrawn at resignation.

Personal circumstances vary. Check with a financial advisor to see what is right for you.

Reference: Annotated LES

Disclaimer

This content is provided for informational purposes only and does not constitute financial, tax, or investment advice. Always consult a qualified professional to review your individual situation and ensure you receive guidance tailored to your needs.

Get Help With Your Retirement

If this helped demystify Box #19, you'll get even more value from the rest of the articles in The Final Muster, where we break down LES line items, benefits, and retirement decisions in plain language.

For deeper, one-on-one help—especially if you're planning a retirement, changing agencies, or weighing resignation versus deferred retirement—reach out to Mark Brown at High 3 Team.

Contact Mark Brown:

- Website: high3team.com

- Email: markbrown@high3team.com

Written by

Mark Brown

Retirement & Benefits Contributor

Founder of High3Team.com, Mark Brown has spent over 22 years helping federal employees with complex, non-traditional careers navigate retirement. From High-3 calculations and FERS quirks to military buybacks and TSP strategy, Mark has guided hundreds of retirees, including CIVMARs, through the maze of federal benefits with clarity and care. Mark has personally visited 22 MSC ships, meeting with mariners around the world to help them take control of their post-sea future. Now, he brings that expertise to CIVSail with a monthly column answering your most pressing retirement questions.

Stay in the Loop

Get new editorials, tools, and mariner resources delivered to your inbox.

No spam, unsubscribe anytime. We respect your inbox.