Don't Let Your SCD Delay Your Retirement

Understand how Box #11 on your LES and Box #31 on your SF-50 affect your leave, TSP vesting, and pension eligibility — and what to do if they're wrong.

Mark Brown

October 31, 2025 · 9 min read

Your Service Computation Date (SCD) is a critical detail on your LES (Leave and Earnings Statement) and one of the least understood. Box #11 "SCD Leave" determines when you can retire, how much leave you earn, and even your standing in a reduction in force (RIF).

Think of it as the government's official clock tracking how long you have been in "creditable" federal service.

Understanding Creditable Service

Creditable service is the time the government counts toward your retirement eligibility and pension calculation. Not every day you work will fit that definition.

Creditable service includes any period where you had retirement deductions withheld from your pay or later made a deposit to cover that time (for example, a military buyback or a re-deposit for prior withdrawn FERS contributions).

Time without deductions — like temporary appointments, intermittent work, or more than six months of LWOP in a calendar year — does not count unless you have paid to make it so.

Location on LES — Box #11

Location on SF-50 — Box #31

Creditable service includes any period where you had retirement deductions withheld from your pay or later made a deposit to cover that time (for example, a military buyback or a re-deposit for prior withdrawn FERS contributions).

Time without deductions — like temporary appointments, intermittent work, or more than six months of LWOP in a calendar year — does not count unless you have paid to make it so.

Types of Service Computation Dates

There are four different SCDs, and each one serves a unique purpose.

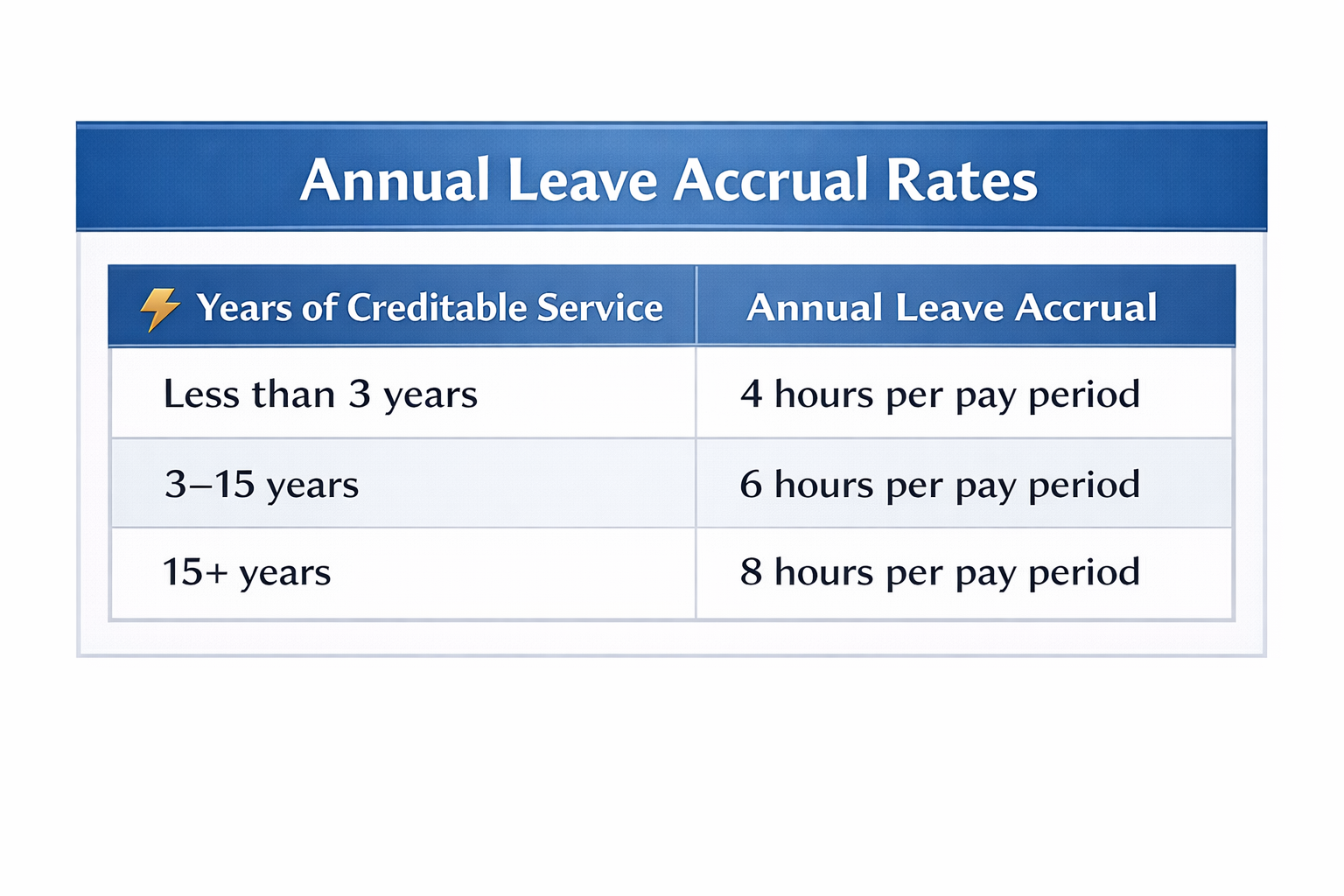

1. SCD for Leave

This is the one that appears in Box #11 on your LES. It determines how much annual leave you earn per pay period:

- Less than 3 years — 4 hours per pay period

- 3–15 years — 6 hours per pay period

- 15+ years — 8 hours per pay period

Tip: This SCD usually includes most of your prior creditable federal and military time (as long as it counts toward leave), but it might not match your Retirement SCD.

2. SCD for Retirement

This date determines when you are eligible to retire and how your FERS annuity is calculated. However, not all service counts here. Time spent in:

- LWOP (Leave Without Pay) beyond six months per calendar year, or

- AWOL (Absent Without Leave)

...is not creditable toward retirement.

A Hidden Trap: AWOL and LWOP Errors from Leave Chits

Many CIVMARs inadvertently rack up AWOL or LWOP simply because their leave chits are filled out incorrectly. The Shoreside Pay System (HRMS) follows a strict hierarchy.

Example: Say you request 5 days of shore leave but only have 3 days on the books. Here's what happens:

- It uses your 3 shore days first (as per your leave chit)

- Then automatically starts charging annual leave once shore leave is gone

- Once annual leave is gone — it defaults straight to AWOL, not LWOP

To use LWOP, you need to elect LWOP on the form.

It works the other way too. If you request 40 hours (5 days) of annual leave but only have 8 hours available, the system will not pull from your shore leave balance. Once that one day is used, the remaining four are charged as AWOL — even though you had leave on the books!

Why It Matters for Retirement

Both AWOL and excess LWOP (anything beyond six months in a calendar year) do not count toward your creditable service. Over a 20-year career, even a few small gaps can push your Service Computation Date forward — meaning you could find yourself weeks or months short of qualifying to retire.

Picture this: you finally get off your "last ship," only to find out HR's math says you owe one more.

If you think MSC's Detailers or HR are going to track down ten-year-old leave chit mistakes so your retirement paperwork comes out clean, that's adorable. They will not. Handle it now, while it's in your control!

Pro Tip: Use the CIVSail Leave Chit Calculator to make sure your leave is entered correctly the first time. It will automatically add LWOP when your leave runs out.

3. SCD for TSP (Thrift Savings Plan)

This date marks the start of your federal service for purposes of vesting in the government's TSP contributions.

- You are fully vested after 3 years of civilian service

- Your own contributions are always yours — vesting applies to the government's matching contributions

4. SCD for RIF (Reduction in Force)

This one comes into play during a Reduction in Force or agency downsizing. On your LES, the SCD for Leave/RIF is typically what is displayed by default. It determines your retention standing compared to other employees.

It factors in all creditable civilian and military service, and in some cases, performance ratings can give you extra retention credit.

Think "last hired, first fired" — and that date is determined by SCD RIF.

What Counts Toward an SCD

Depending on which SCD we're talking about, any of the following may count:

- Temporary, intermittent, part-time, or seasonal service

- Term appointments

- Military service (non-retired)

- Retired military time — if you make a military buy-back and waive your retired pay

- Up to 6 months LWOP per calendar year

- Unlimited USERRA military service

- OWCP time (Workers' Compensation) beyond 45 days

- Career-conditional or career-appointed time

- Cadet Shipping Time — Yes, if you cadet shipped with MSC, that time counts!

Those days can accrue faster than you think and can directly impact your Service Computation Date and help you accrue leave faster if you eventually join MSC full time.

Military Buy-Backs (Briefly)

If you served in the military, you can buy back your active-duty time to count toward your civilian retirement eligibility. It can be a beneficial move, but the timing, process, and details matter. We'll break this down in detail in an upcoming Final Muster article.

FERS Refunds and Broken Service

If you previously left government service and took a FERS refund, that time no longer counts until you make a re-deposit. That means if you resigned, pulled your money out of FERS, and later rejoined, your SCD might reset — unless you pay it back.

For more information on FERS refunds, see our article on Box #19 for a deeper dive.

For retirement eligibility, the ONLY periods that count (Creditable Service) are:

- Time periods that employee contributions were made to CSRS/FERS

- Time periods in which a deposit was made into CSRS/FERS (such as military time)

- Time periods in which a re-deposit is made if CSRS/FERS retirement contributions were withdrawn (resignations/broken service time)

Scenario Examples

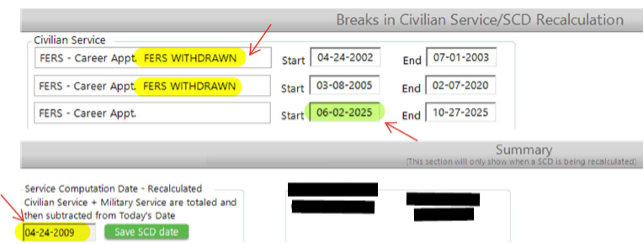

Scenario #1: Broken Service with FERS Withdrawals

In this example, the federal employee has resigned from service twice and returned a third time. The employee withdrew their FERS retirement contributions both times (Box #19/LES).

The employee's LES & SF-50 shows a Service Computation Date of 04/24/2009. This date is calculated by combining the total years/months/days of the two previous periods of service and adding backwards from their third EOD (Entrance of Duty) date.

This SCD of 04/24/2009 is:

- ✅ Correct for RIF, leave accrual, and TSP vesting (if funds were not withdrawn)

- ❌ Incorrect for creditable time for retirement eligibility

Unless the employee makes a re-deposit for the two periods of prior service, their SCD for retirement eligibility and FERS retirement computation is 06/02/2025 (the third EOD).

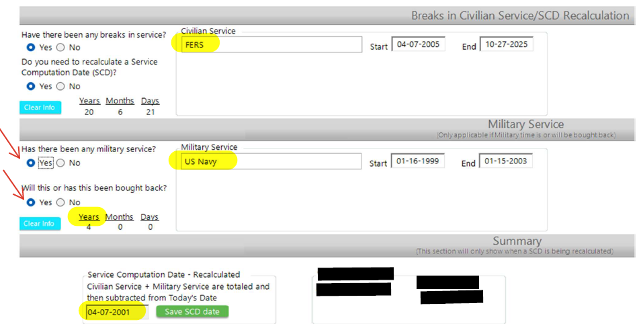

Scenario #2: Military Deposit Made

The employee's LES shows a Service Computation Date of 04/07/2001.

- ✅ Correct for RIF, leave accrual, and TSP vesting

- ✅ Correct for creditable time for retirement eligibility — since the employee made a deposit for four years of military time

Otherwise, their retirement eligibility SCD would be 04/07/2005. If the military deposit has not been made, the SCD on their LES and SF-50 would still display 04/07/2001.

Note: In addition to often being a "value advantage" by increasing this individual's FERS retirement annuity by 4% of the High-3 average, the deposit for military service instantly moves this individual four years closer to creditable service time requirements. It is quite common for a CIVMAR to have the required years of creditable service but not the required age for retirement eligibility.

The Bottom Line

Your first retirement eligibility date depends on your age and years of creditable service.

Once you know that, you can begin estimating your High-3 average and projected monthly annuity — but not before. I have worked with too many employees who discovered — often on their intended retirement day — that they were not eligible to retire yet.

Don't let that be you.

You can find the various Service Computation Dates applicable to you on the GRB Platform. If you have "broken service" or have worked for other Federal Agencies, there may be errors with your SCD(s). The common reason is that the employee's Official Personnel File did not completely transfer to the new Agency, or there were past consolidations like MSC had in 2014.

Final Thoughts

Understanding your SCD is not optional — it is the foundation of your career timeline. Whether you are planning a retirement, considering a resignation, or just trying to figure out how much leave you should be earning, it all starts here.

Retirement math does not care about intentions — only dates. If your record's off, your check will be too. If you don't fix it now, you'll feel it later.

Get Help With Your Retirement

If this article helped demystify Box #11, explore the rest of The Final Muster series on CIVSail.com, where we break down LES line items, benefits, and retirement topics in plain language.

For one-on-one help — especially if you're approaching retirement, changing agencies, or piecing together service history — reach out to Mark Brown.

Contact Mark Brown:

- Website: high3team.com

- Email: markbrown@high3team.com

Written by

Mark Brown

Retirement & Benefits Contributor

Founder of High3Team.com, Mark Brown has spent over 22 years helping federal employees with complex, non-traditional careers navigate retirement. From High-3 calculations and FERS quirks to military buybacks and TSP strategy, Mark has guided hundreds of retirees, including CIVMARs, through the maze of federal benefits with clarity and care. Mark has personally visited 22 MSC ships, meeting with mariners around the world to help them take control of their post-sea future. Now, he brings that expertise to CIVSail with a monthly column answering your most pressing retirement questions.

Stay in the Loop

Get new editorials, tools, and mariner resources delivered to your inbox.

No spam, unsubscribe anytime. We respect your inbox.